Stuff I thought about last week 8-25-19

Welcome to Stuff I Thought About Last Week, a collection of topics on tech, innovation, science, the digital economic transition, the finance industry, crocodile-hunting drones, and whatever else made me think last week. Please grab me on Twitter with any thoughts or feedback. -Brad

Topics in SITALWeek #207: Amazon’s video-streaming blindspot; demographic impacts on restaurants; as Hong Kong protesters topple lamp posts with facial recognition cameras and Huawei struggles to build semiconductors without the help of US and European companies, Trump is backing China into a hard corner that could force their hand to take control of Taiwan; business leaders pledge to do more, but non-zero-sum thinking requires a cultural shift; RV sales and classic car auction declines are telling us something important about the economy; a documentary questions who really is The Amazing Johnathan? And, lots more below.

Click HERE to SIGN UP for SITALWeek’s Sunday EMAIL (please note some ad blocking software may disrupt the signup form; if you have any issues or questions please email sitalweek@nzscapital.com)

Stuff about Innovation and Technology

Hackers can determine your passwords from the sounds of your typing: “Using the microphone found on a smartphone, the new method is so effective that it can be carried out in a noisy public space where multiple people are typing...”

The Little Ripper Group in Australia is using its shark-spotting drone technology to avert croc attacks. The system, which leverages algorithms running on AWS to identify 16 different types of marine animals (including those hard-to-spot crocs lurking below the surface) can also sound sirens, deploy flotation devices, and send live video to rescuers.

A University of Toronto professor is developing an app that can measure blood pressure via a selfie video using existing phone sensors.

Data centers owned by companies will drop to 28,500 in 2020 from 35,900 in 2018 while cloud and co-located data centers will grow from 7,500 to 10,000 over the same period according to this WSJ article. As the shift to the cloud continues, some companies are putting a portion of their remaining legacy data center workloads in co-located facilities, such as those owned by Equinix and Switch, to enable faster connections to cloud platforms. The long-term trend is clear: workloads will largely reside in the cloud and the market for legacy data center hardware will melt away.

Amazon’s manifesto has always been to focus on customers not competitors, but when it comes to video streaming, Bezos seems to have a blindspot. Amazon Prime Video Emmy awards might sell more light bulbs, but, as Fire TV increasingly becomes a platform to resell other people’s content, is Amazon’s $6B in content spending a good use of capital? Amazon has about half of the efficiency of Netflix’s content spending, which results in 20% of the streaming traffic. Further, Bezos has let commercial tension with competitors cloud his judgement on Amazon Fire TV hardware to the detriment of customers. He recently relented and put YouTube back on Fire TV devices, but customers gained nothing from its absence. Disney+ is conspicuously missing from Fire TV despite launching on every other major platform, which also seems to go against Amazon’s customer-first philosophy. Based on my personal usage, consumers still desperately need a neutral platform to provide good universal search and UI as video apps proliferate; Amazon’s strategy is not likely to fill this need. A better use of Amazon's capital might be to acquire a Hollywood studio (or two), or strike exclusive distribution deals with content owners.

Eminem’s publisher sued Spotify, alleging shortfall in payments for his song catalog while implying potential unconstitutionality of the Music Modernization Act. I continue to monitor the low NZS, or lack of win-win, in the relationship between music streaming platforms, publishers, and artists. It’s not usually a good sign to be sued by the suppliers that you rely on. I know earnings have shifted to live performing for many singers, but it seems like music as a loss leader is still a concern for the streaming platforms that aren’t part of Google, Apple, or Amazon. Music streaming platforms are trying to create ancillary revenue opportunities, but I remain skeptical. Related: I find it helpful to refer to podcasts as radio instead of something new and unique. Podcasts are just the digital transformation of the 20th-century broadcast radio model, and will eventually pull in a combination of the radio ad budgets (more valuable with targeting) and some subscription elements. Variety covers the growing digital transformation of radio, i.e., podcasts, in this article.

We were pleased to see the CEOs of the Business Roundtable, including Apple, JP Morgan Chase, Walmart, and hundreds more, discuss the need to go beyond shareholder value this week. We try hard to not be cynical, so, at least for now, we will take them at their word; however, it will be a big cultural shift for companies to embrace this new mentality. We discussed the need for a broader definition of fiduciary duty – beyond shareholder returns – in our whitepaper: NZS - Non-Zero Outcomes in the Information Age. It not only underpins our entire framework for investing, we also think it’s the way for companies to be successful in the 21st century. It goes far beyond ESG and highlights the vulnerability of companies that don’t make this transition. Here is an excerpt from our NZS whitepaper:

Transparency is rising and the velocity of information requires a focus on long-term non-zero-sum-maximizing decisions. Those decisions often, paradoxically, do not maximize traditional measures of shareholder returns in the short term, but will create bigger and stronger companies longer term that have an ability to more positively impact society and the environment. This critical type of thinking requires a high degree of mindful and conscious decision making with longer time horizons. Reorienting a corporate culture toward a long-term decision making framework is crucial to success, and that reorientation must start at the top of an organization and align incentives all the way down to impact even the smallest of decisions. We argue to take into account your employees, customers, suppliers, and the broader environment and social consequences and simply ask the question: “Are we creating more value for our constituents than for ourselves?”

Restaurants, delivery, and demographics: after I wrote last week about various demographic forces shaping the economy for the next decade – namely the accelerating retirement of boomers (whose consumption will drop from $60k/year to $35k/year from around age 55 to age 75), the delayed household formation of Millennials, and the smaller stuck-in-the-middle generation X – I got to thinking about how this will impact the massive disruption starting to impact restaurants and grocery stores. First, we will have declining consumption and shift in eating-out patterns for retiring boomers. Second, we have digital-native Millennials who will likely embrace delivery and bundles/subscriptions for food. Third, we have the rise of cloud kitchens providing higher quality food and more variety without the need for labor- and rent-intensive physical locations. One thing seems very certain: the landscape of restaurants and grocery stores, and how we eat in general, will be unrecognizable ten years from now. I would throw out all prior assumptions and identify 1) platforms that will create network effects, and/or 2) food-provider business models that will be able to plug into those platforms without losing their own economics (brand and habit may become more valuable for some chains). People will still eat out, there will be winners, and some existing restaurants/chains might make the transition, but it’s a wide range of outcomes from here with a lot of profit pools up for grabs. The FT covered the restaurant revolution this week and noted some interesting stats e.g., there are 338M delivery-app users in China, and Beijing alone sustains 1.8M meal deliveries a day.

Huawei is trying to develop alternatives to chip design software Cadence and Synopsys as a result of US bans on technology shipments. In this article, Huawei’s deputy chairman falsely claims Cadence and Synopsys have only been around 10 years, and he says Intel designed chips without these two companies. Perhaps if Wikipedia weren't censored in China, he might learn that Cadence was founded in 1988, Synopsys in 1986, and Intel, along with every other chip maker, now heavily relies on the two software makers. If a country feels beholden to a couple of companies, as is apparently the case with China and Cadence/Synopsys, I’d say that’s a ringing endorsement of how important those businesses are globally. I also think Cadence and Synopsys are relatively high-NZS businesses in our investment framework: they are creating much more value for their customers than themselves. DARPA has looked at open sourcing parts of chip design software, but it’s so far not a popular idea in the industry. Careers of tens of thousands of engineers and nearly every chip we rely on are built on these tools. Even if Huawei were to build their own design software, they would still need Taiwan Semi to make their advanced chips. As a result, Trump appears to be forcing China’s hand over Taiwan (see also Macro Section, below) – the escalating trade war is increasingly looking like it could become an all-out war, and, as I've noted in the past, Taiwan is the ultimate chess piece, especially with their own presidential election coming in 2020 that could push them closer to Chinese control. Will the rest of the world allow a military takeover of Taiwan by China? It appears that's what China is doing – with our tacit permission – in Hong Kong right now. Here is an excerpt from SITALWeek #186:

So, China needs Taiwan and the West needs Taiwan. The West can scramble to build semi fabs, packaging, and testing facilities on US and European soil. For China, they need Taiwan at all costs as leverage. Will the US enter a war to save Taiwan’s sovereignty, or will we instead rely on Korea, Japan, and our semi companies in the US? Even if China takes control of Taiwan’s supply chain, they need design software from Cadence, Synopsys, and the equipment to make chips, which is all made by US and European companies. It’s a mess, and it’s going to get messier! The important takeaway for investors is that semis are the heart of the future of AI, IoT, 5G, etc. – i.e., central to the entire digital economy – and they are only becoming more vital and valuable with accelerating profit pools.

The big Hot Chips semiconductor conference this week saw record attendance and a video presentation from Huawei – after the presenter was denied a visa to attend in person. Chiplets were a hot topic: the architecture allows semi makers to combine multiple functions in one package in order to work around the problems of the slowing of Moore’s Law. “What makes these new architectures so compelling is the ability to customize them for specific applications, leveraging architectures that serve as a foundation for this kind of customization. All of the processor vendors are adopting these types of architectures, from FPGA vendors to companies like Nvidia, which rolled out a new chip architecture in a record-breaking six months...This is just the beginning of a shift that ultimately will involve the entire semiconductor supply chain.”

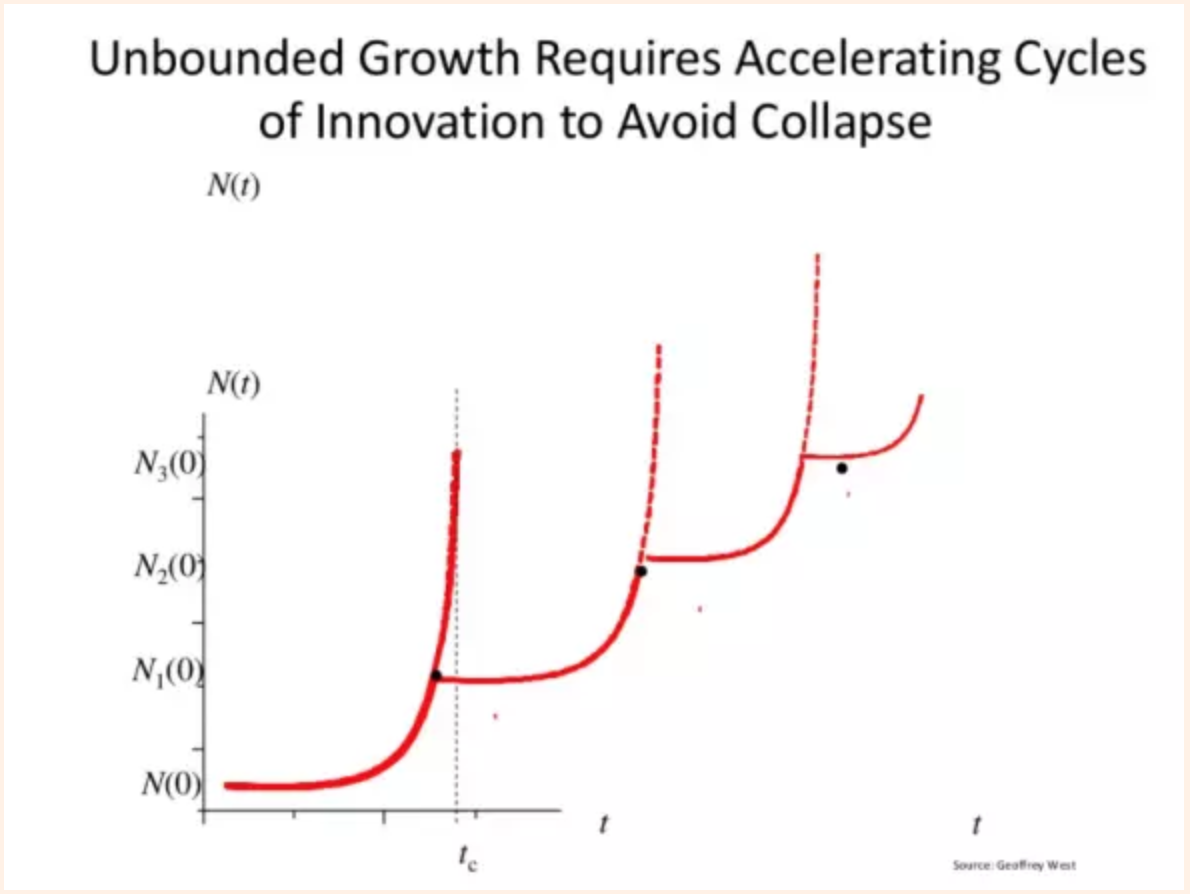

Brinton and I posted a new piece on Stewart Brand’s ‘Pace Layers’ mental model as it relates to the pace of technology disruption and government regulation. The velocity and transparency of the Information Age has allowed technology to have rapid impacts on commerce, infrastructure, and even culture, biology, and geology. Governments have been playing catch up, but they are now at the table and ready to regulate. This means big tech platforms may keep their resilient FCF streams, but they probably can’t stack new growth curves on top on them. Check out the new paper from NZS Capital here.

Miscellaneous Stuff

“Biographies are but the clothes and buttons of the man. The biography of the man himself cannot be written.” This Mark Twain quote leads me to a discussion of The Amazing Johnathan, a comedy magician you might know of or remember (here is a video of a 1995 performance). He was wildly successful for a couple of decades until he retired from performing after a terminal heart diagnosis. Or, did he? One thing we know for sure about magicians: they lie. All the time. Now streaming on Hulu is a film titled The Amazing Johnathan Documentary. But is it a documentary? The film premiered to great reviews at Sundance; but, something’s not quite right about it. I think. Now, a second documentary about The Amazing Johnathan has been released, and it tells a slightly different story, which has made me reassess some of what I thought was real in the first documentary. And, are there two more documentaries yet to be released? Is The Amazing Johnathan trying to tell us something about the relationship between documentarian and their subject? Or was he just cashing in on the documentary-streaming gold rush as he cashes out his own life? Did he get his own mom and David Copperfield to lie about his meth addiction, or is that bit true? Whenever you watch a documentary, you are mostly watching the perspective the documentarian takes, and, at best, you are seeing the clothes and buttons of the subject – that’s something to keep in the front of your mind whenever you sit down to watch your next documentary. This all reminds me of Bob Dylan’s recent Rolling Thunder Revue “documentary” directed by Martin Scorcese, which appeared to be more of a comment on the “post-truth” era of the world than anything else (I wrote briefly on that film in SITALWeek #198). If this sounds at all interesting, I recommend starting with the The Amazing Johnathan Documentary on Hulu followed by Always Amazing on YouTube (apologies to all my international readers, distributions of the Hulu film hasn’t gone international yet, but hopefully you can track it down).

Yahoo Finance writes about Coke and Pepsi’s desire to start shifting plastic water bottles to aluminum. There are 500B PET water bottles made per year compared to 300B cans. Even a small shift would require massive changes and investment, which would obviously be a huge tailwind to the aluminum can industry, as I’ve noted before. Here’s Ball Corp’s CEO from their Q2 earnings call: "if there was going to be a move in the water and there are certainly conversations about that, it'll require some significant collaboration...we'll have to add capacity...I think single serve waters' 500 billion units and global cans is 300. So a 2% move, 3% move would require a very different investment pattern for us."

Boomers are selling Colorado luxury ranches as a generation that grew up enamored with the draw of the West no longer wants the difficult-to-maintain properties. Boomers own 40% of homes in the US, which could impact values as they retire.

Stuff about Geopolitics, Economics, and the Finance Industry

A couple of off-the-beaten-path recession indicators caught my attention recently. I had planned to write about the slowdown in RV sales this week and put it in the context of demographic trends, but the WSJ beat me to it with this article. RV and travel trailer sales were very good early indicators of the 2001 and 2009 recessions, and so far shipments to dealers are tracking down 20% after a 4% drop in 2018; while tariffs aren’t helping the situation, I don't think they are having that significant of an impact on sales. Referencing my write-up on demographics last week, we are approaching the inflection point of boomer retirement: only around 1/3 of boomers have retired and about 35M are still set to retire over the next decade; probably more than a few have dreams of hitting the open road, which will make for one long, continuing tailwind for RV and travel trailer sales. At the same time, the industry is working hard to cater to the rising number of Millennials interested in glamping and the RV lifestyle trend. And, with self-driving technology coming over the next few years (at the very least lane control and parking assistance), RV road trips could become much easier and more fun. So, I'm not seeing any structural demand changes that would explain slowing sales. Yet, Thor, which has about 40-50% share in RVs and towables, has seen their share price drop to $43 from a peak of $153 in 2017. I should note that they also did a sizeable acquisition in Europe, taking their debt burden up, which obviously is going to create volatility for their equity. The company produced a very informative slide deck on their business and the industry that you can read here. A little less dramatic, Winnebago has seen their stock drop from $55 to $32 over the same time period. Of note: other companies exposed to the tailwind of RV usage are Equity Lifestyle Properties and Sun Communities, which own portfolios of RV parks for permanent and transient residents along with their large portfolios of mobile home parks. These stocks are REITs, which tend to be inversely correlated with the drop in interest rates as investors seek yield. Equity Lifestyle and Sun Communities have also been beneficiaries of the housing affordability issues that drive demand for manufactured homes, so their performance has been the opposite of Thor and Winnebago of late.

The 2nd off-the-beaten-path recession red flag I saw this week was the results of the Monterey Car Auctions. These industry-leading, bellwether auctions saw their biggest drop since 2001, with total volume of classic cars sold declining by $120M (34%) from 2018. Combined with the drop in RV sales, these data suggest that a savvy group of boomer consumers aren’t feeling too hot about the current economy. Recessions are reflexive – to borrow a term from George Soros – so fear of recessions can actually manifest them.

I’m rather chagrined to have written so much about macro and interest rates this year. For new readers of SITALWeek, it’s worth mentioning that 1) I put macro in this newsletter last because I don’t think it should be part of long-term equity investors’ process (except to be aware of cycles as we’ve learned from Howard Marks!); and 2) I’m not qualified to comment on macro; indeed, many of my readers are much more knowledgeable on these topics! That said, interest rates to some degree dictate the rate of return you should expect from riskier assets, so they are the one macro data point worth having some opinion on. So, what about these negative rates? Our favorite professor of ergodicity, Ole Peters, argued two years ago in this post that geometric Brownian motion (with an adjustment factor for taxes) is an excellent predictor of what has happened with wealth redistribution under capitalism for the last century. Specifically, he can model what happened starting around 1980 using historical data. He posits that the 35-year decline in rates (driving the 35-year bull market for bonds) has been necessary so that lower-income households can effectively continue to mortgage their futures to fund the shift in wealth to high-income households. This isn’t intended to be a political statement, it’s simply the math of Brownian motion behind many natural phenomena and complex systems, using historical data as input (geometric Brownian motion was discovered in the 1800’s and later defined mathematically by Einstein in 1905; the model describes the random interactions of things such as molecules and has surprisingly broad applications). That said, Peters’ conclusions might not be correct, as his model still relies on human assumptions. Nonetheless, it’s an intriguing and explanatory theory, and it would suggest, absent significant government welfare intervention, we should expect rates to keep going more and more negative. This again supports the view that it might be much more effective for the central banks of the developed world to write checks to households instead of cutting rates further. Both strategies print money, but the former solves inequality, which would boost interest rates and growth. I want to reiterate there is no political statement here, it’s a function of looking at a useful mathematical model and what it might suggest.

One more macro indulgence on interest rates for this week: If we hypothesize that deflation is going to accelerate as a result of technology (productivity, AI, alternative energy, low-capital-intensity/high ROIC businesses of the Information Age, etc.), then we can also explain lower and lower negative rates. Why? If I think I only need 90 cents five years from now to buy stuff that would cost $1 today, then I’m happy to invest my money in negative-rate debt and I still come out ahead if I only get back 95c on those bonds.

So, I’ve just gone over two factors potentially driving increasingly negative rates. And, it’s possible that deflation and rising inequality are having a tandem effect on interest rates that could be stabilized with government-led welfare or spending. I highly recommend that Ole Peters post (and don’t get bogged down in the math, just focus on the context he provides for falling rates). I believe technological innovation will continue to garner a large share of the value created in the global economy. If wealth redistribution is stabilized or reversed, you should expect higher rates, but deflation from technological forces will likely still be at play. As a result, you have to assume that if rates go back up, it probably won’t be by much, which leaves the expected return hurdle rate for investments quite low.

As recession indicators pile up and rate fears continue, it’s worth noting that investors, and humans, tend to become greedy slowly over time, but they become fearful very quickly. There’s good evolutionary explanation for this, and I’d keep it in mind as the reflexive nature of the economy causes a slowdown and market correction: "be greedy when others are fearful" as Buffett often says, and don’t forget the power of economic cycles. Odds strongly favor that things will be better 10 years from now; and 10 years after that they will be even better...

Schwab’s subscription-based advisor service (monthly fee, not based on percent of assets) is said to have raised $1B in Q2, 37% from new clients. As I’ve mentioned in the past, the breakeven for clients on this service is well over $100K in assets.

Before Trump labeled Xi an enemy of the US on Friday and ordered US companies to find alternatives to China, Twitter and Facebook took down thousands of Chinese-state-controlled accounts that were spreading misinformation on the Hong Kong protests. Hong Kong protesters toppled smart lamp posts this weekend in an attempt to disable facial recognition cameras. The image of the falling lamp posts recalls the toppled Saddam Hussein statues – both visions of humans taking back their freedom.Following up on my warning last week that any Chinese or HK company should be treated as a state-owned entity from a risk perspective, I have to say that the actions of the ousted Cathay Pacific airlines CEO were quite commendable: when China asked for a list of Cathay employees that participated in the HK protest, he responded by listing "self" and no one else. Cathay's flight attendant union leader was also dismissed. Cathay – and any other business controlled by China that relies on Westerners for revenue – is facing a tough future. And, the protests have caused Alibaba to postpone their HK listing, which was likely a precursor to de-listing in the US: Hong Kong may no longer a stable place for the global financial markets.

This Pew study shows that US citizens’ views on China have turned sharply negative as ongoing rhetoric is preparing people to support an escalation of tensions, if one should occur.

Disclaimers:

The content of this newsletter is my personal opinion as of the date published and are subject to change without notice and may not reflect the opinion of NZS Capital, LLC (“NZS”). This newsletter is simply an informal gathering of topics I’ve recently read and thought about. It generally covers topics related to the digitization of the global economy, technology and innovation, macro and geopolitics, as well as scientific progress, especially in the fields of cosmology and the brain. I will frequently state things in the newsletter that contradict my own views in order to be provocative. I often I try to make jokes, and they aren’t very funny – sorry.

I may include links to third-party websites as a convenience, and the inclusion of such links does not imply any endorsement, approval, investigation, verification or monitoring by NZS Capital, LLC (“NZS”). If you choose to visit the linked sites, you do so at your own risk, and you will be subject to such sites' terms of use and privacy policies, over which NZS Capital has no control. In no event will NZS be responsible for any information or content within the linked sites or your use of the linked sites.

Nothing in this newsletter should be construed as investment advice. The information contained herein is only as current as of the date indicated and may be superseded by subsequent market events or for other reasons. There is no guarantee that the information supplied is accurate, complete, or timely. Past performance is not a guarantee of future results.

Investing involves risk, including the possible loss of principal and fluctuation of value. Nothing contained in this newsletter is an offer to sell or solicit any investment services or securities. Initial Public Offerings (IPOs) are highly speculative investments and may be subject to lower liquidity and greater volatility. Special risks associated with IPOs include limited operating history, unseasoned trading, high turnover and non-repeatable performance.